List To Floor Assertion

Financial Statement Analysis Example Financial Statement Analysis Financial Statement Analysis

9 Assertion Hallway Concepts That Will Deliver The Thoroughfare To Life 2020 In 2020 Living Room Reveal Beach House Decor Hallway Decorating

Pin On Customer Experience

Chapter 9 Audit Procedures

Pin On For Me Resilience

Distinct Furniture Along With Modern Pattern Makes An Assertion In Your Home Come Across Present Day Settees Areas And Me Home Home Remodeling House Interior

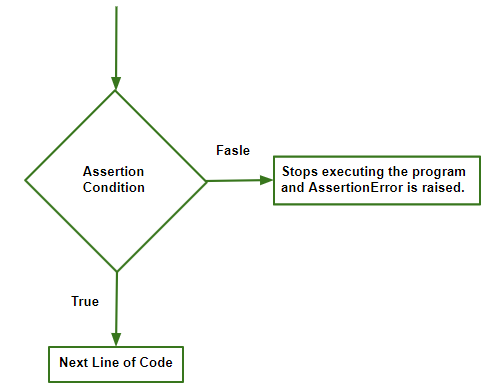

The six assertions that you must attend to when auditing occurrence ownership completeness authorization accuracy and cutoff are outlined here occurrence.

List to floor assertion. The assertion of accuracy and valuation is the statement that all figures presented in a financial statement are accurate and based on proper valuation of assets liabilities and equity balances. During your audit you need to test management financial statement assertions for fixed and intangible asset transactions. For example in order to think you typically begin with what you know to be true the following are illustrative examples of assertions. This assertion is critical for the asset accounts because it is a reflection of the strength of the company.

An assertion is described by an assertion descriptor. In addi tion to the components of every constraint descriptor an assertion. In preparing financial statements management is making implicit or explicit claims i e. Assertions regarding the recognition measurement and presentation of assets liabilities equity income expenses and disclosures in accordance with the applicable financial reporting framework e g.

The auditors test the validity of these assertions by conducting a number of audit tests. To test the occurrence of. Management assertions are claims made by members of management regarding certain aspects of a business. It refers to the fact that the assets the liabilities and the equity balances mentioned in the books exist at the end of the accounting period.

This is a basis for logic thought processes and systems. 4 10 4 assertions an assertion is a named constraint that may relate to the content of individual rows of a table to the entire contents of a table or to a state required to exist among a number of tables. List of audit assertions related to account balances 1 existence. The concept is primarily used in regard to the audit of a company s financial statements where the auditors rely upon a variety of assertions regarding the business.

Occurrence tests whether the fixed asset transactions actually took place. The assertions form a theoretical basis from which external auditors develop a set of audit procedures. All of the information cont. These assertions are as follows.

Python Assertion Error Geeksforgeeks

100 Opposite Words List Antonym Vocabulary Example Sentences In 2020 Opposite Words Opposite Words List Vocabulary

A Literary Review Is A Summary About A Specific Topic In Essay Form Contains A Apa Re Argumentative Essay Creative Writing Workshops College Admission Essay

Small Bathroom Design Photos Low Budget Small Bathroom Design Photos Low Budget Small Bathroom In 2020 Budget Bathroom Remodel Bathrooms Remodel Diy Bathroom Remodel

Https Comptroller Defense Gov Portals 45 Documents Fiar Fiar Guidance Pdf

Profit And Loss Statement Self Employed Profit And Loss Statement Statement Template Budgeting Worksheets

Wandfarbe Apricot Flur Gestalten Floraler Teppichl Ufer Decorstyle Entrywaydecor Decorsmall In 2020 Narrow Entryway Decor Foyer Decorating Hallway Designs

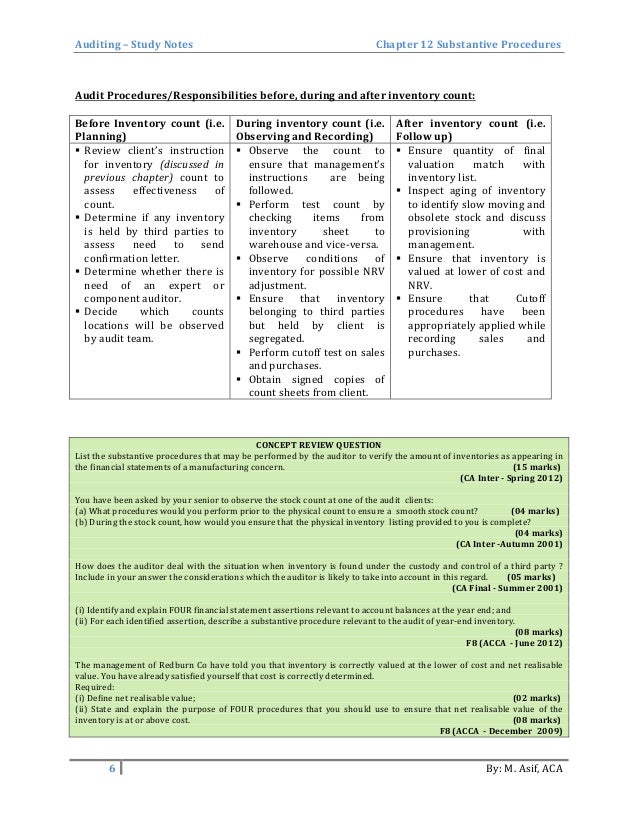

Substantive Procedures Auditing Study Notes

Public Mind Map By Tyler Smith Create Your Own Collaborative Mind Maps For Free At Www Mindmeister Com Mind Map Eos Tyler Smith

Ana Book Blogger On Instagram How Do You Guys Store Your Books Towering Bookshelves Or Stacke In 2020 Study Room Decor Bookshelves In Bedroom Room Ideas Bedroom

Distinct Furnishings Along With Advanced Plan Makes An Assertion In Your Home Look Up New Chairs Mattress And Sto Murphy Bunk Beds Bunk Beds Murphy Bed Plans

A Visit To Rumson Vintage House Plans Luxury House Plans Rumson

Check Out These Out Of This World Approaches With Regard To A Triple Bunk Bed Space Bunkbedcabin Bunk Beds Triple Bunk Beds Modern Bunk Beds

No Ordinary Saugling S Room Baby Room Safari Room Room

100 Laminate Sheets Manufacturers Price List Designs And In 2020 Laminate Sheets Laminate Hardwood

Https Www Acq Osd Mil Pepolicy Pdfs Assertion Package Outline Final Pdf

Red Carpet Birthday Celebration Cubicle Office Birthday Decorations Office Birthday Cubicle Birthday Decorations

Whether Or Not You Want To Make A Bold Assertion Otherwise You Merely Wish To D Bedroom Wallpaper Accent Wall Accent Walls In Living Room Wallpaper Accent Wall

3

Distinct Furniture By Using Contemporary Plan Makes An Assertion In Your Home Find New Chairs Bed Fr Interior Design Home Interior Design Trendy Living Rooms

20 Paulo Coelho Quotes That Will Lift Your Spirit Good Thoughts Quotes Inpirational Quotes Wisdom Quotes

40 Trendy Farmhouse Master Bedroom Design Ideas The Tall White Curtains H In 2020 Farmhouse Style Master Bedroom Stylish Master Bedrooms Rustic Master Bedroom

Promatz Dungeon Floor Theme Terrain Game Mat Flooring Theme Table Games

Dark Sash With Images Interior Design Kitchen Kitchen Interior Mediterranean Kitchen

Metal Wall Art That Makes A Statement Steel Wall Art Decor Metal Wall Art Decor

Pin On First Birthday Ideas

Pin By Carmen Putnam On Wish List House With Porch Screened Porch Doors Porch Design

Chivalrous Enlarged Bathroom Renovating Ideas Pop Over To This Site Bathroomrenovatingideas In 2020 Flooring For Stairs Bathrooms Remodel Bathroom Makeover

Pin On Furniture

You Can Find The Latest Trends About Living Room Decor Here And At Our Website See More At Spotools Com Modern Modular Homes

Liquid Rainbow By Edwin Deen Painting Liquid Rainbow Big Art

How To Declare 5 Main Problems To Fix Before And After You Move In 2020 Home Declutter Declutter Your Home

15 Luxury Living Room Designs Stunning Modern Interior Design Modern Interior House Design

Anne Lindberg The Red List Museum Of Contemporary Art Unusual Art Sculpture Installation

Polsterbett Leonas 160x200cm Weiss Design Bett Mit Beleuchtung Home Room Design Bed Bedroom Design

Innovative Quick Step Laminate Flooring At Amazing Prices With Its Trademark Easy Fit Uniclic Design Free Delivery Laminate Flooring Flooring Laminate

Exceptional Furniture By Using Current Pattern Makes An Assertion In Your House Look Up New Sofas Area Kitchen Mirror Kitchen Design Kitchen Trends

Gazebo Plans Woodworking Plans Woodworking Ideas Woodworking Lathe Diy Santa Christmas Woodworking Pdf Delta Woodworking Toddler B Woodworking Plans Woodworking Basics Gazebo Plans

Y2k Aesthetic Institute Recent Interior Design Finds See Added Captions Design Interior Design Interior

One Of A Kind Home Furnishings With The Use Of Modern Plan Makes An Assertion In Your House Come Across Modern Day Couches B Circle Bed Bed Design Round Beds

Spanish Farmhouse Design 99 Inpiration Photos 99architecture Home Decor Home Interior

Pecos House Austin Texas Von Jaycorderarchitect Interiorsmagazine Finearchi Modern House Design House Design Decor Interior Design

Large Angler Malvertising Campaign Hits Top Publishers Malwarebytes Labs Malwarebytes Publishing Angler